Smart Money Concepts: The Ultimate Guide to Trading Like Institutional Investors

Learn how institutional investors compound their wealth through strategic market positioning and patience.

Are you a visual learner? Check out this YouTube video where I cover what compound interest is, how it works, and why Einstein called it the 'eighth wonder of the world.' I'll walk you through real examples, share interactive calculators, and demonstrate how even small investments can grow to life-changing sums through the power of compounding.

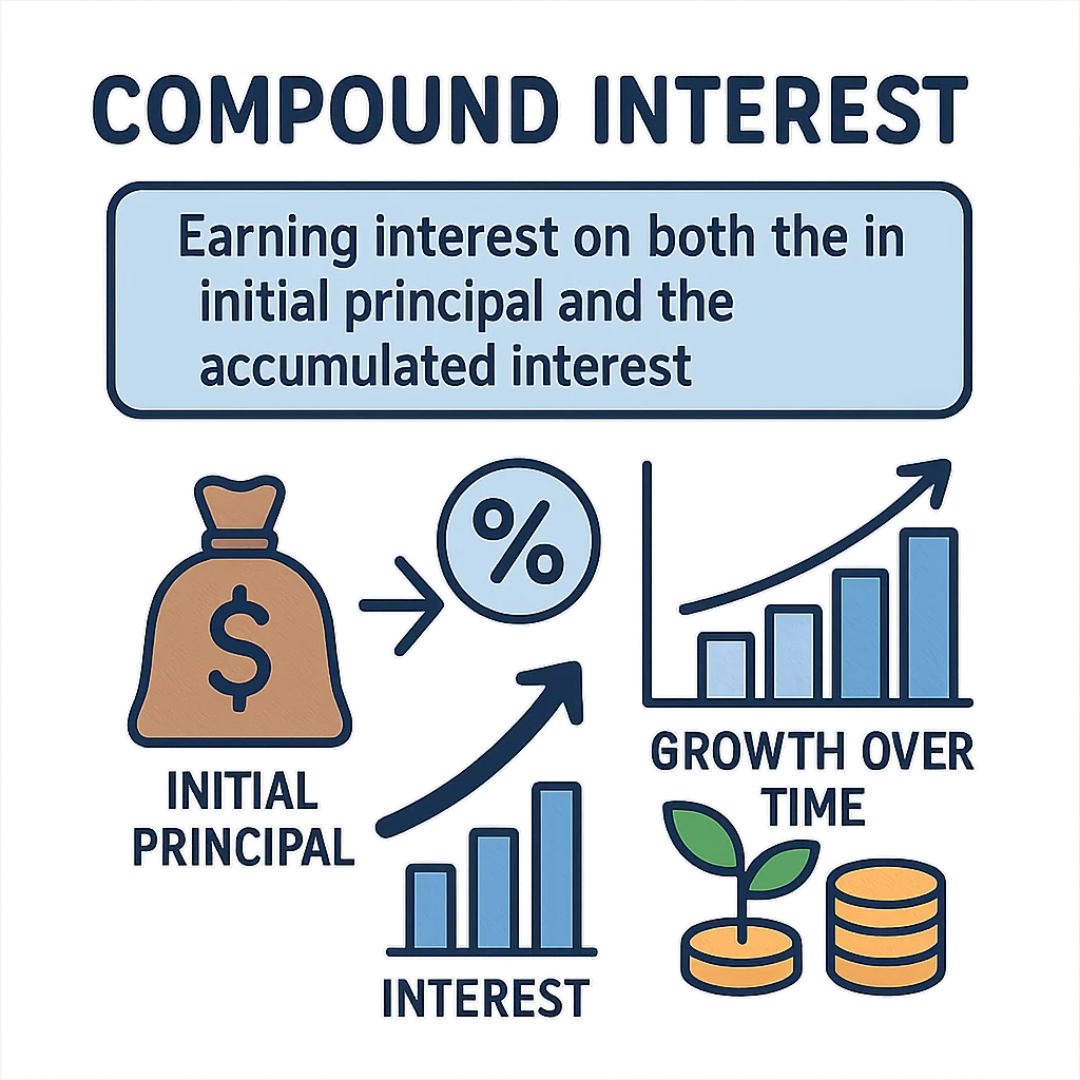

Compound interest is the process of earning interest on both your initial investment and on previously earned interest, creating exponential growth over time.

The power of compound interest relies primarily on three factors: time, rate of return, and consistent contributions—with time being the most crucial element.

Even small differences in rates of return can lead to dramatically different outcomes over long time periods due to the exponential nature of compound growth.

Dollar Cost Averaging (DCA) is a powerful investment strategy that combines well with compound interest by reducing risk, averaging purchase prices, and building financial discipline.

Starting early, automating investments, reinvesting returns, and focusing on maximizing your rate of return are key strategies to harness the full potential of compound interest.

Compound interest will make you rich—and it's not magic, it's simply mathematics. This powerful financial concept has been called the "eighth wonder of the world" by none other than Albert Einstein, and for good reason. Today, we're diving deep into what compound interest is, how it works, and most importantly, how you can harness its incredible power to build wealth over time.

Compound interest, in simple terms, is the principle of earning interest on both your initial principal (the money you start with) and on the interest that your money has already earned. This creates a snowball effect where your money grows faster and faster over time.

Let's look at a simple example to illustrate this concept:

Imagine you invest $100 that grows by 10% annually. After the first year, you've earned $10 in interest, bringing your total to $110. In the second year, that 10% growth applies to the entire $110, giving you $11 in interest (instead of just $10). Your new total becomes $121.

This might seem small at first glance—just $1 extra—but this is where the magic begins. As your balance grows, that same percentage yields increasingly larger amounts. This is the essence of what financial experts call "interest on interest."

Compound interest is when you earn interest on both your initial investment and the accumulated interest over time. It's interest-on-interest that creates exponential growth, building upon previous growth as shown in this curve comparison.

Compound interest leads to exponential growth, which is fundamentally different from linear growth. Most things we encounter in everyday life follow linear patterns, which is why exponential growth often feels magical or counterintuitive.

Here's why exponential growth from compound interest is so powerful:

Exponential vs. Linear Growth: Rather than growing at a steady, predictable rate (like adding $10 every year), compound interest creates a curve that starts slowly but accelerates dramatically over time.

Time Amplifies Growth: The longer your money compounds, the faster it grows. Patience isn't just a virtue when it comes to compound interest—it's the primary ingredient.

Frequency Matters, But Less Than You Think: More frequent compounding (monthly instead of yearly) helps, but time and rate of return are much bigger factors in the long run.

Small Rates Yield Massive Results: Even relatively modest rates of return can lead to impressive sums given enough time. This is perhaps the most magical aspect of compound interest.

To truly understand the power of compound interest, let's examine how a $100 investment would grow at different annual rates of return:

Looking at this table, the difference becomes clear. After 10 years, the 20% annual return yields over $619 from an initial $100 investment—more than 6 times your initial amount. Meanwhile, the 5% return only yields about $163. This demonstrates why investment returns are so critical to long-term wealth building.

Now, let's scale up and see how compound interest can create truly life-changing wealth. With the right combination of time, rate of return, and initial investment, the results can be staggering.

Imagine investing $1,000 with an annual interest rate of 20% (a very good rate of return for long-term investing). Here's how it would grow over time:

After 10 years: $6,191

After 20 years: $38,337

After 30 years: $237,376

After 40 years: $1,469,772

After 50 years: $9,100,438

That's right—$1,000 can grow to over $9 million in 50 years at a 20% annual return. While achieving a consistent 20% return over decades is challenging, this example illustrates the raw power of compound interest.

If we increase the annual return to 30% (which is exceptional performance), that same $1,000 could theoretically grow to over $500 million in 50 years. This might seem unbelievable, but it's simply the mathematical reality of exponential growth.

This calculator uses monthly compounding. Results are rounded to the nearest dollar.

While compound interest is powerful on its own, combining it with a disciplined investment approach called Dollar Cost Averaging (DCA) can enhance your results even further.

DCA is an investment strategy where you invest a fixed amount regularly—for example, $100 per month or $100 per week—regardless of market conditions. This approach has several significant advantages:

It reduces risk: By spreading your investments over time, you avoid the danger of investing everything at market peaks.

You average out your purchase price: Sometimes you'll buy when prices are high, sometimes when they're low, which typically results in a favorable average price over time.

It builds investment discipline: When you commit to investing regularly, you remove much of the emotion from investing and develop healthy financial habits.

Let's look at a practical example:

Starting with an initial investment of $1,000 and adding $100 every month with an estimated annual return of 10% (a reasonable long-term average for stock market investing), here's how your investment would grow:

After 10 years: Total invested: $13,000. Estimated value: $23,513

After 20 years: Total invested: $25,000. Estimated value: $75,937

After 30 years: Total invested: $37,000. Estimated value: $217,097

After 40 years: Total invested: $49,000. Estimated value: $596,254

After 50 years: Total invested: $61,000. Estimated value: $1,615,875

The power becomes even more evident with a higher return rate. At 30% (though this is extremely optimistic for long-term investing), that same strategy would yield approximately $74 million after 50 years—from a total investment of just $61,000.

While many investors understand the basic concept of dollar cost averaging, several key benefits are often overlooked:

Risk reduction beyond market timing: DCA doesn't just help you avoid buying at market peaks—it fundamentally changes your relationship with market volatility. When prices drop, your regular investment actually buys more shares, setting you up for greater gains when the market recovers.

Psychological benefits: Perhaps the greatest advantage of DCA is psychological. By establishing a consistent investment routine, you remove the emotional decision-making that destroys many investors' returns. You know that every month on a specific date, you'll invest a predetermined amount—no questions, no second-guessing.

Compound interest acceleration: By continuously adding new capital that immediately begins compounding, you create multiple "layers" of compound interest working simultaneously. This accelerates your overall returns beyond what a single lump-sum investment would achieve.

Simple interest is calculated only on the initial principal amount, while compound interest is calculated on both the initial principal and the accumulated interest from previous periods. For example, with a $1,000 investment at 10% interest, simple interest would earn you $100 each year consistently. With compound interest, you'd earn $100 in year one, $110 in year two, $121 in year three, and so on, as the interest itself begins earning interest.

While more frequent compounding (daily, monthly, quarterly) does lead to slightly higher returns compared to annual compounding, the difference is relatively small compared to the impact of time and rate of return. Most investments compound annually or quarterly, but the most important factors for growth are: 1) starting early to maximize time, 2) achieving the highest reasonable rate of return, and 3) consistently adding new capital to your investments.

The Rule of 72 is a simple mathematical shortcut to estimate how long it will take for an investment to double at a given interest rate. Simply divide 72 by the annual interest rate to get the approximate number of years. For example, at 8% interest, an investment will double in approximately 9 years (72 ÷ 8 = 9). This rule provides a quick mental calculation to understand the power of compound interest without using complex formulas.

Statistically, investing a lump sum tends to outperform Dollar Cost Averaging about two-thirds of the time in rising markets, simply because money is invested sooner. However, DCA offers significant psychological benefits by reducing the impact of volatility and regret if markets decline shortly after investing. DCA is particularly valuable for investors who: 1) are worried about market timing, 2) have regular income rather than a large lump sum, or 3) are emotionally affected by market swings. The best approach often depends on your personal circumstances and risk tolerance.

Achieving consistent 20-30% annual returns over long periods is extremely difficult and exceeds the performance of most professional investors. The long-term average return of the S&P 500 stock market index is closer to 10% annually. The examples using 20-30% returns are primarily to illustrate the mathematical power of compound interest rather than suggesting such returns are easily achievable. For most investors, focusing on broad market index funds, consistent contributions, low fees, and a long time horizon is a more realistic approach to building wealth through compound interest.

The ideal amount to invest regularly depends on your financial situation, goals, and timeline. A common guideline is to aim for 15-20% of your income, but even small amounts like $50 or $100 per month can grow significantly over time thanks to compound interest. The most important factors are consistency (investing regularly), starting early (giving your money more time to compound), and gradually increasing your contributions as your income grows. Remember that compound interest rewards patience—even modest investments can grow substantially over decades.

Understanding compound interest and dollar cost averaging is just the beginning of your financial journey. Here are some concrete next steps to put these powerful concepts to work:

Start now: The most important factor in compound interest is time. Even if you can only invest a small amount, beginning today gives you a tremendous advantage over waiting.

Automate your investments: Set up automatic transfers to your investment account on a regular schedule. This ensures you stick with your dollar cost averaging plan without having to make repeated decisions.

Focus on increasing your rate of return: While always balancing with appropriate risk management, look for investment opportunities that can deliver higher returns. Even a small increase in your average return can make an enormous difference over decades.

Reinvest all returns: Make sure dividends, interest, and other returns are automatically reinvested rather than taken as cash. This maximizes the compound effect.

Increase your contributions over time: As your income grows, gradually increase your regular investment amount. This accelerates your wealth building without requiring dramatic lifestyle changes.

Compound interest truly is the eighth wonder of the world—a mathematical principle with the power to transform modest investments into life-changing wealth. The key ingredients are time, consistency, and patience. Start today, stay the course, and let the magic of compounding work for you.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The example returns used are for illustrative purposes and may not reflect realistic market conditions. Always consult with a qualified financial advisor before making investment decisions.

Learn how institutional investors compound their wealth through strategic market positioning and patience.

Discover value investing principles that maximize long-term compound growth from the father of value investing.

Learn how AI-powered tools can help you find high-growth investments to maximize your compound returns.

Explore how cryptocurrencies could potentially fit into a diversified compound interest investment strategy.

(Limited Time: Save 70% Today!)

Discover stocks with growth potential to maximize your compound interest returns.

(Limited Time: Save 70% Today!)

Advanced algorithms identify investments with strong compound growth potential.

(Limited Time: Save 70% Today!)

Build a balanced portfolio designed for maximum compound growth over time.

I bought my first stock at 16, and since then, financial markets have fascinated me. Understanding how human behavior shapes market structure and price action is both intellectually and financially rewarding.

I’ve always loved teaching—helping people have their “aha moments” is an amazing feeling. That’s why I created Mind Math Money to share insights on trading, technical analysis, and finance.

Over the years, I’ve built a community of over 200,000 YouTube followers, all striving to become better traders. Check out my YouTube channel for more insights and tutorials.